Stunning Closing Entries For Retained Earnings Lufthansa Financial Statement

What Are Retained Earnings Guide Formula And Examples

Accountants will debit the expense account and credit cash. The only entry required to record the appropriation of 25000 of retained earnings to fulfill the provisions in a loan agreement is. To take the actual - minus budget amount and deduct it from retained earnings Its all. The closing entries of a corporation include closing the income summary account to the Retained Earnings account. This is contrary to what is normally done as Bob has made a net loss for the period. All temporary accounts must be reset to zero at the end of the accounting period. If the corporation was profitable in the accounting period the Retained Earnings account will be credited. Therefore this entry will ensure that the balance has been transferred on the balance sheet. The income summary is a temporary account used to make closing entries. To calculate the retained earnings at the.

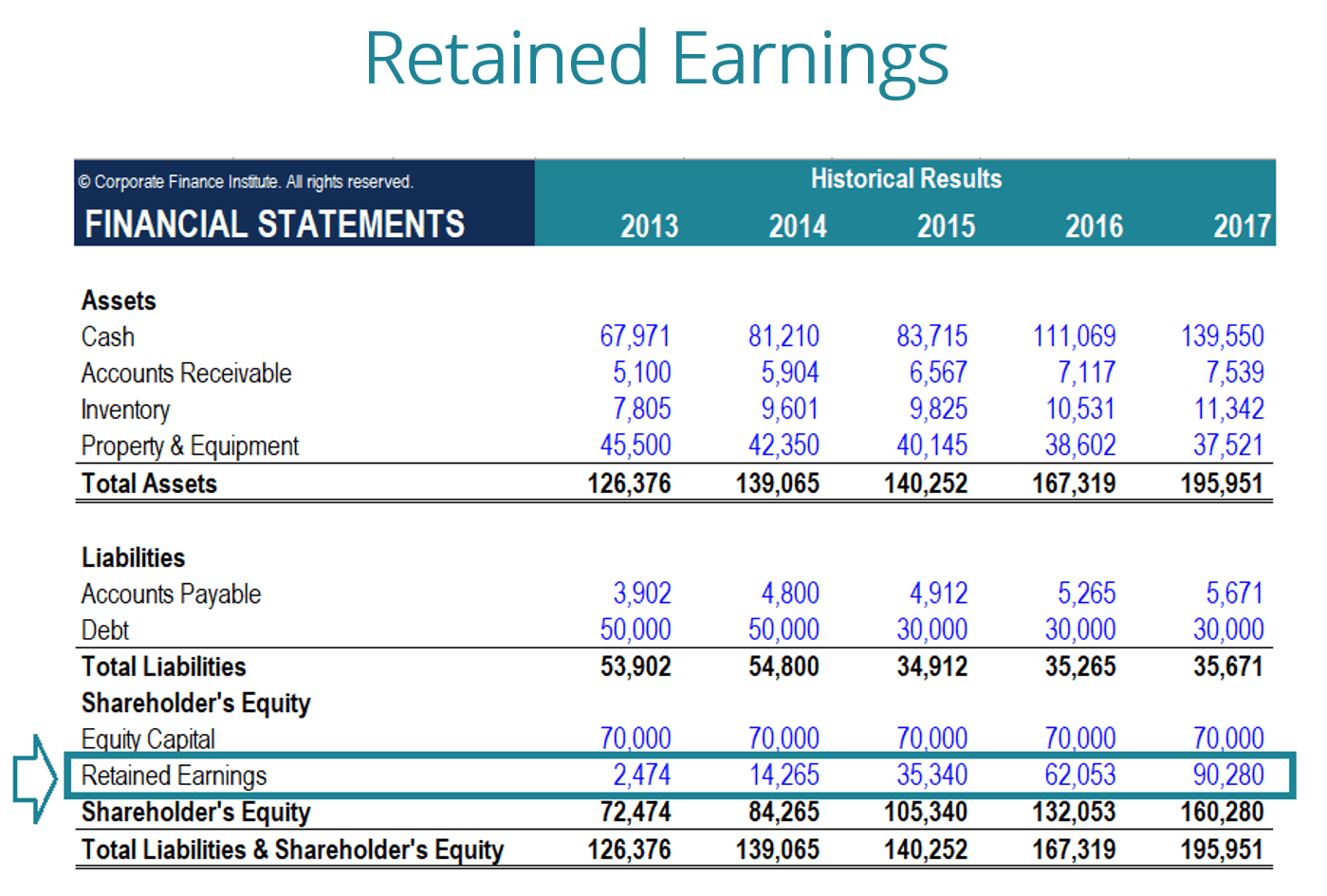

Retained earnings is an account used to represent the accumulated earnings that the business has chosen to reinvest into its operations rather than distribute to its shareholders as dividends.

Closing entries are entries used to shift balances from temporary to permanent accounts at the end of an accounting period. Retained earnings represent the amount your business owns after paying expenses and dividends for a specific time period. Closing Entry 3 for Bob To close the income summary account to the retained earnings account Bob needs to debit the retained earnings and credit the income summary. Closing Entries to Retained Earnings - YouTube. 4000 in net income at the end of the period. To take the actual - minus budget amount and deduct it from retained earnings Its all.

The closing entry process accomplishes two tasks. Retained earnings change in each period of the businesss operation as a function of the businesss net income and the dividends that it declares. Dr Retained earnings Cr Sales. For example a closing entry is to transfer all revenue and expense account totals at the end of an accounting period to an income summary account which effectively results in the net income or loss for the period being the account balance in the income summary account. Closing expenses to retained earnings will be the final entry for this set of. The closing entries of a corporation include closing the income summary account to the Retained Earnings account. Beginning RE of 5000 when the reporting period started. In corporations this entry closes any dividend accounts to the retained earnings account. Closing Entries to Retained Earnings - YouTube. Therefore this entry will ensure that the balance has been transferred on the balance sheet.

Beginning RE of 5000 when the reporting period started. To take the actual - minus budget amount and deduct it from retained earnings Its all. These journal entries condense your accounts so you can determine your retained earnings or the amount your business has after paying expenses and dividends. In corporations this entry closes any dividend accounts to the retained earnings account. Dr Sales Cr Retained Earnings. Closing retained earnings Statement of retained earnings It reports figures for any adjustment to opening retained earnings net income or net loss for the period and cash dividends or stock dividends ie. Then you shift the balance in the income summary account to the retained earnings account. Accountants will debit the expense account and credit cash. The purpose of the income summary account is simply to keep the permanent owners capital or retained earnings account uncluttered. This is contrary to what is normally done as Bob has made a net loss for the period.

Dr Sales Cr Retained Earnings. 4000 in net income at the end of the period. Retained earnings represent the amount your business owns after paying expenses and dividends for a specific time period. This is Not what happens. Closing retained earnings Statement of retained earnings It reports figures for any adjustment to opening retained earnings net income or net loss for the period and cash dividends or stock dividends ie. It enables you to determine net income or retained earnings for the current accounting period and it. Beginning RE of 5000 when the reporting period started. Closing Entry 3 for Bob To close the income summary account to the retained earnings account Bob needs to debit the retained earnings and credit the income summary. Dr Retained earnings Cr Sales. This includes rent utilities and security among other basic costs.

To take the actual - minus budget amount and deduct it from retained earnings Its all. In some cases however a company will need to retain enough cash to pay the final expenses associated with its physical location. For example a closing entry is to transfer all revenue and expense account totals at the end of an accounting period to an income summary account which effectively results in the net income or loss for the period being the account balance in the income summary account. The only entry required to record the appropriation of 25000 of retained earnings to fulfill the provisions in a loan agreement is. Retained Earnings are part which is a permanent account on the balance sheet. All temporary accounts must be reset to zero at the end of the accounting period. It enables you to determine net income or retained earnings for the current accounting period and it. To do this their balances are emptied into the income summary account. Beginning RE of 5000 when the reporting period started. Your entry is a Math computation.

Closing Entries to Retained Earnings - YouTube. Close the owners drawing account to the owners capital account. Beginning RE of 5000 when the reporting period started. The only entry required to record the appropriation of 25000 of retained earnings to fulfill the provisions in a loan agreement is. All temporary accounts must be reset to zero at the end of the accounting period. Retained earnings represent the amount your business owns after paying expenses and dividends for a specific time period. This is Not what happens. The purpose of closing entries is to merge your accounts so you can determine your retained earnings. If the corporation was profitable in the accounting period the Retained Earnings account will be credited. For any year end run the Balance Sheet as of the Next Day.