Or to be on the safe side we use ADEx LER again. The amount calculated is the balancing figure to be put on the debit side as a part of balancing the account. As balance sheet is a statement and not an account so there is no debit or credit side. After cash dividends are paid the companys balance sheet does not have any accounts associated with dividends. Debits must always be on the left side or left column and credits must always be on the right side or right column. The totals of these two sides should be equal. When the company pays dividends it debits this account which reduces shareholders equity. How to Calculate the Balances To begin enter all debit accounts on the left side of the balance sheet and all credit accounts on the right. Whether a debit or credit can either increase or decrease an overall account balance is determined by the account type that is receiving the credit or debit transaction. Ledger accounts may be divided into two main types.

The amount calculated is the balancing figure to be put on the debit side as a part of balancing the account. Include the balance for each. On the asset side of the balance sheet a debit increases the balance of an account while a credit decreases the balance of that account. Or to be on the safe side we use ADEx LER again. The dividend account has a normal debit balance. Whether a debit or credit can either increase or decrease an overall account balance is determined by the account type that is receiving the credit or debit transaction. This means an increase in these accounts increases shareholders equity. How to Calculate the Balances To begin enter all debit accounts on the left side of the balance sheet and all credit accounts on the right. There are two sides of it- the left-hand side Debit and the right-hand side Credit. Accounts that normally have a debit balance include assets expenses and losses.

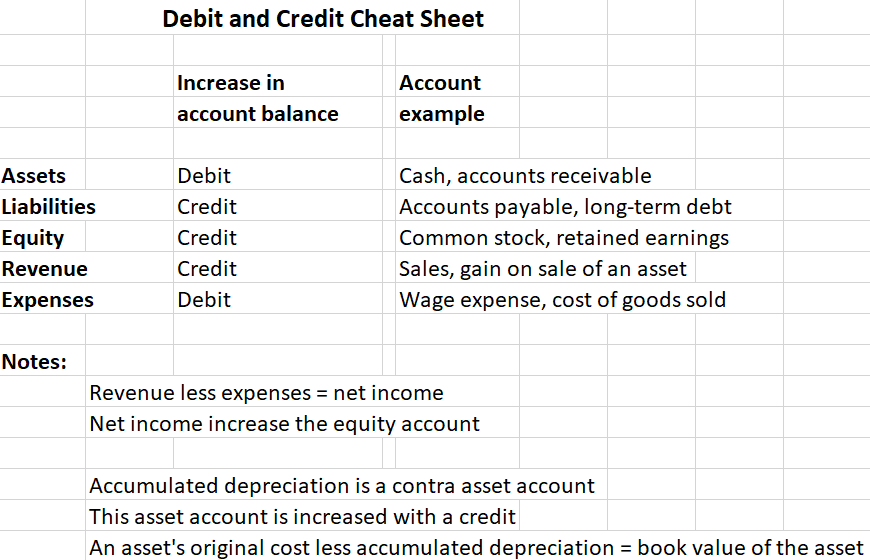

The golden rule in accounting is that total debits must equal total credits. The totals of these two sides should be equal. Include the balance for each. The debit falls on the positive side of a balance sheet account and on the negative side of a result item. How to Calculate the Balances To begin enter all debit accounts on the left side of the balance sheet and all credit accounts on the right. Ledger accounts may be divided into two main types. The term debit refers to the left side of an account and credit refers to the right. In fundamental accounting debits are balanced by credits. When the company pays dividends it debits this account which reduces shareholders equity. The trial balance is a bookkeeping systematized worksheet containing the closing balances of all the accounts.