Top Notch Loss On Disposal Of Non Current Assets Party City Financial Statements

Disposal Of Assets Disposal Of Assets Accountingcoach

Asset Disposal on Financial Statements. During the year to 30th June 20X7 Eugene Ltd sold a non current asset for 36000. Any sale of Non-Current Assets means that Assets need a credit entry to close it and the provision for depreciation needs a debit entry to close it and fully remove the old asset from the books. A question during the year to 30th June 20X7 Eugene Ltd sold a non current asset for 36000. Disposal for cash consideration. The asset disposal results in a direct effect on the companys financial statements. The proceeds of disposal 200 the market-value was less than the carrying-value of the non current asset 400. Another fun feature of asset disposal is the GST or Goods and Services Tax. At the date of disposal of the asset the accumulated depreciation was 138000. B Non-current assets at 31 December 2002 were 290 000.

A Current liabilities at 31 December 2002 were 115 150.

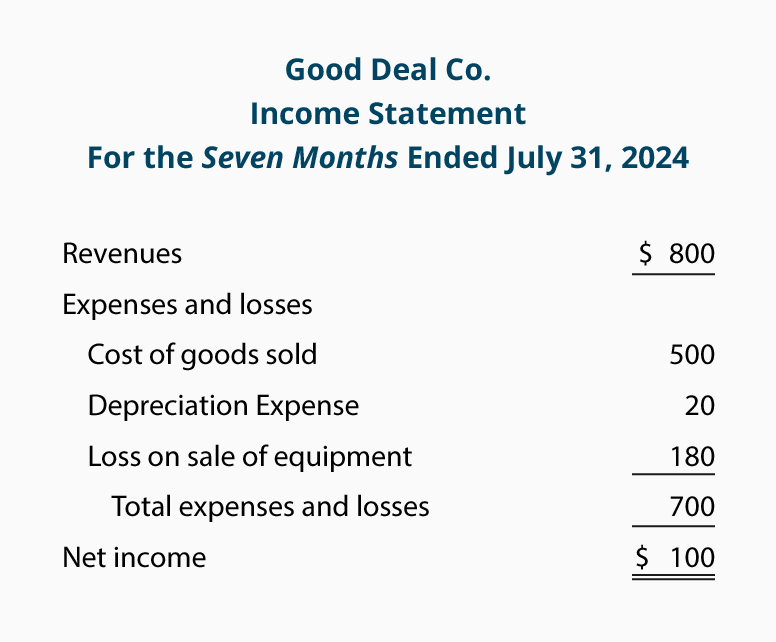

Calculate and record profits or losses on disposal of non-current assets in the statement of profit or loss including part exchange transactions. A loss results from the disposal of a fixed asset if the cash or trade-in allowance received is less than the book value of the asset. The company also experiences a loss if a fixed asset that still has a book value is discarded and nothing is received in return. Another fun feature of asset disposal is the GST or Goods and Services Tax. The main items included in the balance under this heading in the accompanying consolidated income statements are as follows. Asset Disposal on Financial Statements.

During the year to 30th June 20X7 Eugene Ltd sold a non current asset for 36000. Part exchange allowance Instead of receiving sales proceeds as cash a part exchange allowance could be offered against the cost of a replacement asset. This is the difference between the net sale price of the asset and its net book value at the time of disposal. No proceeds fully depreciated. The gain or loss is calculated as the net disposal proceeds minus the assets carrying value. It had been acquired three years ago at a cost of 180 000. This is an income statement account which reflects any profit or loss on disposal. Find profit or loss on depreciation and make journal entries to record the disposal. The proceeds of disposal 200 the market-value was less than the carrying-value of the non current asset 400. The journal entries should be adjusted accordingly.

The proceeds of disposal 200 the market-value was less than the carrying-value of the non current asset 400. Thus there was a loss on the sale. The company also experiences a loss if a fixed asset that still has a book value is discarded and nothing is received in return. This is the difference between the net sale price of the asset and its net book value at the time of disposal. 9 Disposal of non-current assets. Debit all accumulated depreciation and credit the fixed asset. The difference between the two is needed to close the account. A question during the year to 30th June 20X7 Eugene Ltd sold a non current asset for 36000. 521 Gains losses on non-current assets held for sale not classified as discontinued transactions. The assets used in the business can be sold anytime during their useful life.

At the date of disposal of the asset the accumulated depreciation was 138000. Credit Asset disposal account Note. During the year to 30th June 20X7 Eugene Ltd sold a non current asset for 36000. Thus there was a loss on the sale. Since a non-current asset is used over a certain time frame therefore it is advisable to charge the cost of the asset in that time frame. 521 Gains losses on non-current assets held for sale not classified as discontinued transactions. A disposals T account is required when recording the disposal of a non-current asset. Sales proceeds NBV profit on disposal Sales proceeds. Calculate and record profits or losses on disposal of non-current assets in the statement of profit or loss including part exchange transactions. At the date of disposal of the asset the accumulated depreciation was 138000.

At the date of disposal of the asset the accumulated depreciation was 138000. A loss results from the disposal of a fixed asset if the cash or trade-in allowance received is less than the book value of the asset. A question during the year to 30th June 20X7 Eugene Ltd sold a non current asset for 36000. It had been acquired three years ago at a cost of 180000. B Non-current assets at 31 December 2002 were 290 000. Any sale of Non-Current Assets means that Assets need a credit entry to close it and the provision for depreciation needs a debit entry to close it and fully remove the old asset from the books. Loss on disposal arises when the net book value cost of non-current asset less provision for depreciation of the non-current asset sold is. This is an income statement account which reflects any profit or loss on disposal. When a non-current asset is sold there is likely to be a profit or loss on disposal. Debit all accumulated depreciation and credit the fixed asset.

All goods are sold at prices calculated at 15 times the cost of goods sold. ACurrent assets at 31 December 2002 were 130 000. 521 Gains losses on non-current assets held for sale not classified as discontinued transactions. Thus there was a loss on the sale. The main items included in the balance under this heading in the accompanying consolidated income statements are as follows. Since a non-current asset is used over a certain time frame therefore it is advisable to charge the cost of the asset in that time frame. Gains Losses in Non-current Assets Held for Sale. When a non-current asset is sold there is likely to be a profit or loss on disposal. The company also experiences a loss if a fixed asset that still has a book value is discarded and nothing is received in return. Here are the options for accounting for the disposal of assets.