Ace Nature Of Provision For Doubtful Debts Steel Industry Average Financial Ratios

Bad Debt Provision Meaning Examples Step By Step Journal Entries

The journal entry is passed at the year-end by debiting profit and loss account bad debt expense and crediting provision for doubtful debt. The provision for bad debts might refer to the balance sheet account also known as the Allowance for Bad Debts Allowance for Doubtful Accounts or Allowance for Uncollectible Accounts. The provision for doubtful debts is the estimated amount of bad debt that will arise from accounts receivable that have been issued but not yet collected. In conclusion provision or allowance for doubtful debt is an estimated amount of invoices that would be uncollectible. There are a lot of litigations and disputes. Provision for doubtful debts acts as a liability for the business and is shown on the liability side of a balance sheet. A corresponding debit entry is recorded to account for the expense of the potential loss. The provision for doubtful debts or provision for bad debts is different to doubtful debts or bad debts. Browse more Topics under Financial Statements. An Introduction to Financial Statements.

It provides for deduction towards provision for bad and doubtful advances.

Under the accounting standard FRS 39 which sets out the principles for recognising and measuring financial instruments general and specific provisions for bad and doubtful debts will no longer be made. In conclusion provision or allowance for doubtful debt is an estimated amount of invoices that would be uncollectible. The term general is used when there is no clear evidence that which trade receivable will not clear his debt. Provision for bad and doubtful debts general note impairment loss on trade debts Provision for obsolete stocks general Reinstatement costs expenses incurred to reinstate. The journal entry is passed at the year-end by debiting profit and loss account bad debt expense and crediting provision for doubtful debt. Impairment loss is recognized as an expense in the Statement of Financial Performance.

It may be included in. There are a lot of litigations and disputes. It is nothing but a loss to the company which needs to be charged to the profit and loss account in the form of provision. Premises to its original condition prior to vacating. The provision for bad debts might refer to the balance sheet account also known as the Allowance for Bad Debts Allowance for Doubtful Accounts or Allowance for Uncollectible Accounts. 1 General Provision for Doubtful Debts. It provides for deduction towards provision for bad and doubtful advances. Such receivables are known as doubtful debts. The provision is a future loss - a future loss that must be recorded as soon as it becomes likely to. This provision of doubtful debt is a contra asset and hence credit in nature as compared to the accounts receivable that are classified as assets and are debit in nature.

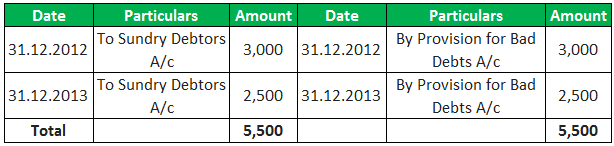

Section 361viia One section which is very relevant for the banking industry is section 361viia. Provision for bad and doubtful debts general note impairment loss on trade debts Provision for obsolete stocks general Reinstatement costs expenses incurred to reinstate. Such receivables are known as doubtful debts. Provision for doubtful debts acts as a liability for the business and is shown on the liability side of a balance sheet. In this case the account Provision for Bad Debts is a contra asset account an asset account with a credit balance. Provision for Doubtful Debts. Provision for Bad Debts Meaning. There are following two types of provision for doubtful debts or allowance for bad debts. Provision for bad debts. If Provision for Doubtful Debts is the name of the account used for recording the current periods expense associated with the losses from normal credit sales it will appear as an operating expense on the companys income statement.

The provision for bad debts might refer to the balance sheet account also known as the Allowance for Bad Debts Allowance for Doubtful Accounts or Allowance for Uncollectible Accounts. In this case the account Provision for Bad Debts is a contra asset account an asset account with a credit balance. In accordance with IAS 39 an objective assessment of financial assets is made at financial year-end in order to determine possible impairment. Section 361viia One section which is very relevant for the banking industry is section 361viia. Prudence requires that an allowance be created to recognize the potential loss arising from the possibility of incurring bad debts. The journal entry is passed at the year-end by debiting profit and loss account bad debt expense and crediting provision for doubtful debt. The provision for doubtful debts is the estimated amount of bad debt that will arise from accounts receivable that have been issued but not yet collected. In conclusion provision or allowance for doubtful debt is an estimated amount of invoices that would be uncollectible. The provision is used under accrual basis accounting so that an expense is recognized for probable bad debts as soon as invoices are. Provision for bad and doubtful debts general Provision for obsolete stocks general Renovation or refurbishment works you may claim Section 14Q deduction for qualifying expenditure incurred Retrenchment payments Ex-gratia retrenchment payments and outplacement support costs where there is a complete cessation of business.

It is identical to the allowance for doubtful accounts. Regarding issue of treating the provision for bad and doubtful debts and bad debts written off as non operating expenses for the purpose of margin computation of comparable companies as selected by the TPO the TPO observed that provision for doubtful debts are considered as operating expenses only when the same expenses are incurred every year for the last three years upto and including FY. Such receivables are known as doubtful debts. Prudence requires that an allowance be created to recognize the potential loss arising from the possibility of incurring bad debts. Accounting entry to record the allowance for receivable is as follows. Under the accounting standard FRS 39 which sets out the principles for recognising and measuring financial instruments general and specific provisions for bad and doubtful debts will no longer be made. The allowance for doubtful debts is created by forming a credit balance which is deducted from the total receivables balance in the statement of financial position. Doubtful debts or bad debts is an expense and has already occurred. Another point to note here is that since these are estimates we are unsure of which invoice would default exactly. The provision for bad debts might refer to the balance sheet account also known as the Allowance for Bad Debts Allowance for Doubtful Accounts or Allowance for Uncollectible Accounts.

Another point to note here is that since these are estimates we are unsure of which invoice would default exactly. The allowance for doubtful debts is created by forming a credit balance which is deducted from the total receivables balance in the statement of financial position. Every year the amount gets changed due to the provision made in the current year. It is identical to the allowance for doubtful accounts. The provision is made on an individual basis or based on expected cash flows. For income tax purposes impairment losses on trade debts that are revenue in nature will be allowed deduction. Here is an attempt to simplify it. There are a lot of litigations and disputes. In accordance with IAS 39 an objective assessment of financial assets is made at financial year-end in order to determine possible impairment. The provision is used under accrual basis accounting so that an expense is recognized for probable bad debts as soon as invoices are.